The prediction market industry wants to be treated as a serious financial product for regulatory classification purposes and as a fun startup when it comes to consumer protection. Canadian regulators should not let them have it both ways.

Key Takeaways:

- The prediction market industry has a serious and demonstrable insider trading problem. The Maduro trade on Polymarket, a $32,000 bet that yielded $400,000 hours before a classified U.S. military operation was announced is not an isolated incident, and Canadian regulators should not wait for a domestic scandal to act.

- Retail participants lose significantly more on prediction markets than in regulated gambling environments. Data shows median users losing roughly 7% of wagers in the first 90 days versus 1% on conventional sportsbooks. This is a gap that widens dramatically at lower performance percentiles, driven by structural informational asymmetry between casual users and professional trading firms.

- Canada has no coherent regulatory framework for prediction markets, and the jurisdictional confusion between federal and provincial authorities is creating a vacuum that Canadians are already filling through VPNs and offshore workarounds. Provincial regulators, not Ottawa, are best placed to act, but speed matters before the U.S. libertarian model becomes the default template.

Prediction markets are having a moment. From their widely discussed role during the 2024 U.S. presidential election to the explosive growth in sports and event-based contracts, platforms like Polymarket and Kalshi have gone from niche curiosities to mainstream financial products in the United States. The recent Golden Globes featured integration into the broadcast and Substack has even announced that creators will be able to insert Polymarket data seamlessly.

There is a reasonable case for prediction markets. At their best, they aggregate dispersed information and produce real-time probability estimates that serve as a useful informational signal to help with decision making. You don’t have to want to bet on an outcome to find the results a useful data point to track. For sophisticated participants, they can also function as hedging instruments for multivariate outcomes, thus allowing firms and individuals to manage exposure to political, regulatory, or economic events that are otherwise difficult to price. In this narrow sense, prediction markets resemble traditional derivatives: tools for risk transfer and price discovery where conventional futures markets do not exist.

But those kinds of real use cases have been overtaken by a much more troubling reality. The prediction market industry is rife with structural problems that are only going to get worse before they get better as a wider universe of dopamine addicted bettors are enticed into the platform through advertising and cross-platform promotion. There are also serious concerns about insider trading and conflicts of interest, along with broader risks of a financial literacy crisis among retail participants, along with mounting evidence that casual users fare worse on these platforms than they do in regulated gambling environments.

We are currently operating with effectively no regulatory guardrails. And even though prediction markets are largely prohibited in Canada, the absence of a clear framework to deal with this phenomenon opens the risk that when Canada flicks a switch to enable them, we will be under pressure to quickly adopt the U.S. approach of libertarianism rather than a more sophisticated understanding of the risks and issues involved.

The insider trading problem is real

In January, a trader on Polymarket placed a bet of roughly $32,000 that U.S. forces would take action against Venezuelan President Nicolás Maduro — hours before the operation was publicly announced. The payout: an estimated $400,000 profit. Rep. Ritchie Torres has since introduced the Public Integrity in Financial Prediction Markets Act of 2026 to ban federal officials from trading on prediction markets related to their duties. It is a start, but barely scratches the surface. This is just one of many such examples across industries and countries in recent years.

In traditional capital markets, insider trading is illegal and vigorously prosecuted. Prediction markets, by contrast, operate in a regulatory grey zone where the rules are still being written. In the U.S., the Commodities Futures Trading Commission (CFTC) has not yet taken an official position on how insider trading provisions apply to event contracts and has also moved to supersede states which are attempting to regulate prediction markets under the guise of gambling. Without clear, enforceable rules that are at minimum equivalent to what exists in securities and derivatives markets, prediction markets will become the most attractive vehicle for corrupt self-dealing since the invention of the stock option.

Readers should take note: the political dynamics that created the Maduro bet are not limited to the U.S. We are not immune to the incentive structures that make this kind of conduct attractive, and we should not wait for a Canadian scandal before addressing the risk. Given that most prediction markets are integrated with crypto trading there is certainly already the possibility that Canadians are circumventing jurisdictional restrictions and engaging in the practice, much as Canadians flocked to grey-market online gaming platforms before this was more directly regulated here at home.

Retail participants are losing badly

The narrative that prediction markets are fairer than traditional gambling because “you’re betting against other people, not the house” has a nice ring to it. It is also misleading.

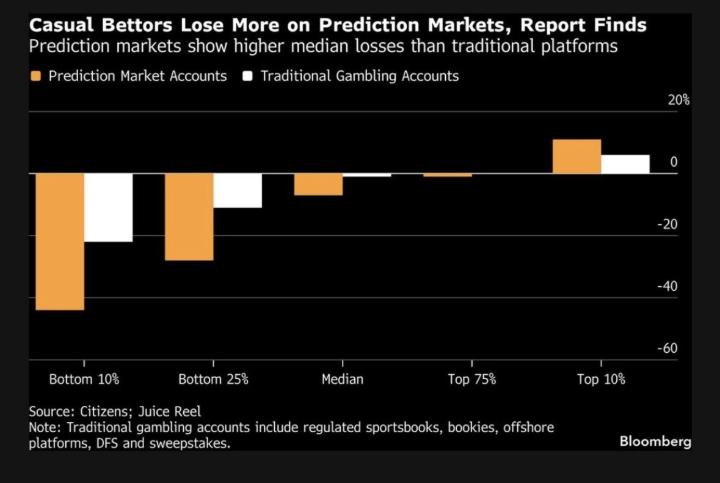

A recent equity research report from Citizens, using data from the analytics firm Juice Reel, found that the median prediction market user lost approximately 7% of their wagers within the first 90 days, compared to roughly 1% on traditional regulated sportsbooks. Among the worst-performing quartile, prediction market participants lost about 28 cents of every dollar wagered in their first three months, compared to 11 cents on conventional platforms. At the bottom decile, losses approached 44%. As the following chart from Bloomberg illustrates, the losses are not just worse — they are dramatically worse at nearly every percentile.

These numbers tell us something important about the structure of these markets. The platforms may not have a “house” in the traditional sense, but they do have sophisticated participants — professional traders, market-making firms, and quantitative funds — who are on the other side of the average person’s bet. The result is a market where informational asymmetry is the defining feature. The average prediction market bet is over $185 — more than triple the $55 average on a regulated sportsbook. Prediction markets are creating worse outcomes for the people who can least afford it, while better-resourced participants capture the difference. That is not price discovery. It is a transfer of wealth from the financially unsophisticated to the financially sophisticated, wrapped in the language of innovation.

A financial literacy quagmire

One illustration of how absurd prediction markets have become: Polymarket now actively features contracts on whether Jesus Christ would return. One such contract peaked at 35% odds of Christ’s return in early February. It is now trading under 1%.

In a post on X (formerly Twitter) earlier this month, I noted that this should serve as a reminder to regulators about the financial literacy problem embedded in these platforms. Think through the logic of that bet. If you are a Christian and you wager that Jesus returns, the theological implications of collecting are rather existential. And if you vote “No,” you are essentially giving Polymarket an interest-free loan of your cash until the contract expires.

The platform collects transaction fees regardless. People do not understand this. These platforms are blurring the line between investing, gambling, and entertainment in ways that make it very hard for the average person to understand what they are actually doing with their money.

Canada’s regulatory vacuum

Here in Canada, the situation is arguably worse, not because our markets are more dangerous, but because we have essentially no framework at all. There is no enabling legislation, court ruling, or regulatory decision that explicitly permits prediction markets to operate. But there is also no coherent plan for what to do about them.

Provincial and federal officials cannot even agree on what prediction markets are. The Canadian Securities Administrators banned short-term binary options in 2017 in a move motivated by widespread fraud in the retail binary options industry. In 2025, the Ontario Securities Commission determined that Polymarket’s event contracts violated that order and blocked the platform in the province. The federal Department of Finance has punted to the provinces, characterizing prediction markets as “gambling activities.” Alberta’s gaming regulator says they are prohibited under current rules but is working with partners to determine a regulatory approach as the province prepares to launch its open iGaming market (for a good overview read this recent piece in Canadian Affairs). The Alcohol and Gaming Commission of Ontario has declined to comment.

This is a vacuum, and in the meantime, Canadians are already accessing these platforms through offshore workarounds and VPNs. We are regulating nothing while activity grows.

The jurisdictional confusion is particularly Canadian. Under the Criminal Code, gambling is prohibited unless conducted and managed by the provinces. Private operators can only participate through provincial licensing regimes, like Ontario’s iGaming framework or the new Alberta model. But if prediction markets are classified as derivatives rather than gambling, they fall under securities regulation and the CSA’s binary options prohibition. And if they are crypto-settled, as Polymarket’s are, that adds another layer of regulatory complexity.

This matters especially now because Canada’s online gambling landscape is going through a significant transition of its own. Ontario’s competitive iGaming market launched in 2022, generating billions in monthly wager volume and establishing the most advanced regulated online gambling framework in the country. Alberta is expected to open imminently. The Canadian Gaming Association just released a new responsible advertising code effective January 2026. Into this evolving picture, prediction markets arrive as an unregulated product competing for the same consumer dollars under none of the same consumer protections, responsible gambling obligations, or tax treatment.

For the Carney government, which has demonstrated both a willingness to assert federal jurisdiction over digital finance — as it did with the Stablecoin Act — and a general instinct toward market-based regulatory frameworks that set clear rules without banning entire categories of activity, prediction markets pose some interesting questions.

I do not necessarily favour any federal regulation, arguably provincial securities and gambling authorities are well placed to sort this out. But speed is important. It is conceivable that as federal parliamentarians continue down the road of wanting to more directly regulate how online sports betting is advertised and regulated – there have been several private members bills in this space (one such example) – stakeholder groups will push for federal intervention more broadly. And it could also become codified into a federal approach to online harms. Provincial regulators need to get on with the business of developing a clear and consistent approach.

Innovation is not an exemption from rules

It would likely be foolish for Canadian regulators to ban prediction markets outright. Prohibition pushes activity underground and removes any possibility of oversight. But the current state of affairs, platforms operating with minimal insider trading rules, no standardized investor protection, no financial literacy requirements, and an active dispute over whether they are financial products or gambling, is not sustainable.

At a recent CFTC-SEC summit, Polymarket’s founder argued that regulators should exempt “innovative” platforms from certain rules.

The prediction market industry wants to be treated as a serious financial product when it comes to regulatory classification and tax treatment, but as a fun startup when it comes to oversight and consumer protection. It cannot be both. If these are derivatives, regulate them like derivatives. If they are gambling, regulate them like gambling. Calling something “innovative” is not a regulatory framework. It is a marketing strategy that will inevitably hurt consumers, potentially even more than online sports betting which in some ways we are coming to regret.

Prediction markets can serve a useful purpose in our financial ecosystem. But only if we build the regulatory architecture that ensures they operate fairly, transparently, and without becoming yet another mechanism through which the financially sophisticated extract value from those who are not. We have been here before with every wave of financial innovation — from subprime mortgages to binary options to crypto exchanges. The lesson is always the same: innovation without guardrails benefits the few at the expense of the many. Regulators in Canada and elsewhere have a window to get this right before the next scandal makes the choice for them. They should take it.