In the first of a multi-part series, Tyler Meredith explains and dissects the fundamentals of “Carneynomics.” Part One examines Carney’s revival of fiscal rules.

Key Points:

- Based on the “golden rule” borrowed from the UK, Carney’s goal is to change the composition of spending rather than just the level of spending. Borrowing, in this model, becomes a lever for future capacity, not a tool for present consumption.

- The goal is to shift spending away from operational government expenses and transfers, reversing a national trend of under-investment.

- The shift shows that Carney values fiscal transparency, and ultimately Canadians will have to decide whether they want this shift to spending focused on future productive capacity rather than present consumption.

Get the latest MBP Intelligence briefings in your inbox:

Get MBP Intelligence directly in your inbox

No spam. Unsubscribe anytime.

As the government begins to roll out details of its first major economic and fiscal policy moves, it will be important to step back to assess what we can learn about a “new” government that is still maturing, what they mean in practice and the implications for future policy making. We will ignore the politics and punditry and delve into the details of how this affects public administration, advocacy and policy design.

First up, this past week featured two major changes to the way budgets themselves are put together. One PM Carney campaigned on — changing how public spending is categorized — and another he did not — inverting the calendar of fiscal events so that Budgets are now presented in the fall preceding the next fiscal year, and Updates coming the following spring.

This post deals with the implications of the former: the creation of a new framework for capital and operating spending and its related commitment to balance the operating budget.

In part 2 of this series, I’ll look at the new fiscal calendar and how it will fundamentally transform policy and program design within government.

“Spend Less, Invest More”: Context and Background

While some commentators and opponents scratched their head at Carney’s slogan during the recent election campaign to “spend less, invest more,” the commitment was quite literal.

As now confirmed in government policy, the intention is to shift fiscal policy toward a place where future deficits are only reserved for investments that create future assets or long-term economic value. This isn’t a new idea. In fact, it’s not even a Canadian one. The shift is largely inspired by a series of reforms then UK Chancellor of the Exchequer, Gordon Brown, introduced in 1997 as part of the “golden rule”. The goal then was to arrest the UK’s deficit and ensure that borrowing financed future productive capacity rather than present consumption.

The goal then is to change the composition of spending, rather than the level of spending.

Some critics will argue that “spending is spending” so we should instead target an overall, all-in deficit. Others will also point out that since the government uses a modified form of cash/accrual accounting, it already includes and incentivizes capital spending because accrual accounting looks at capital costs over the lifecycle (depreciation).

The first criticism reflects a fundamental difference of opinion about the role of government in the economy today and what is needed to jolt Canada out of a stasis of lacklustre private sector investment. The second is a reasonable point, but as I’ll discuss below fails to acknowledge that since the federal government often (because of federalism) doesn’t own the assets it helps to fund (e.g. transit systems and affordable housing run by cities and non-profits), a simple accrual framework still undercounts and discourages investment in capital.

Will this Work?

Research from the IMF, the Institute for Fiscal Studies, and scholars such as David Heald and Alasdair McLeod on Brown’s Golden Rule has found that the UK approach succeeded in increasing the UK’s infrastructure and capital share of spending. It was not perfect. Its credibility depended on clearly defining what counted as “investment” and sticking to it. But it established a behavioural norm that helped shift policy culture.

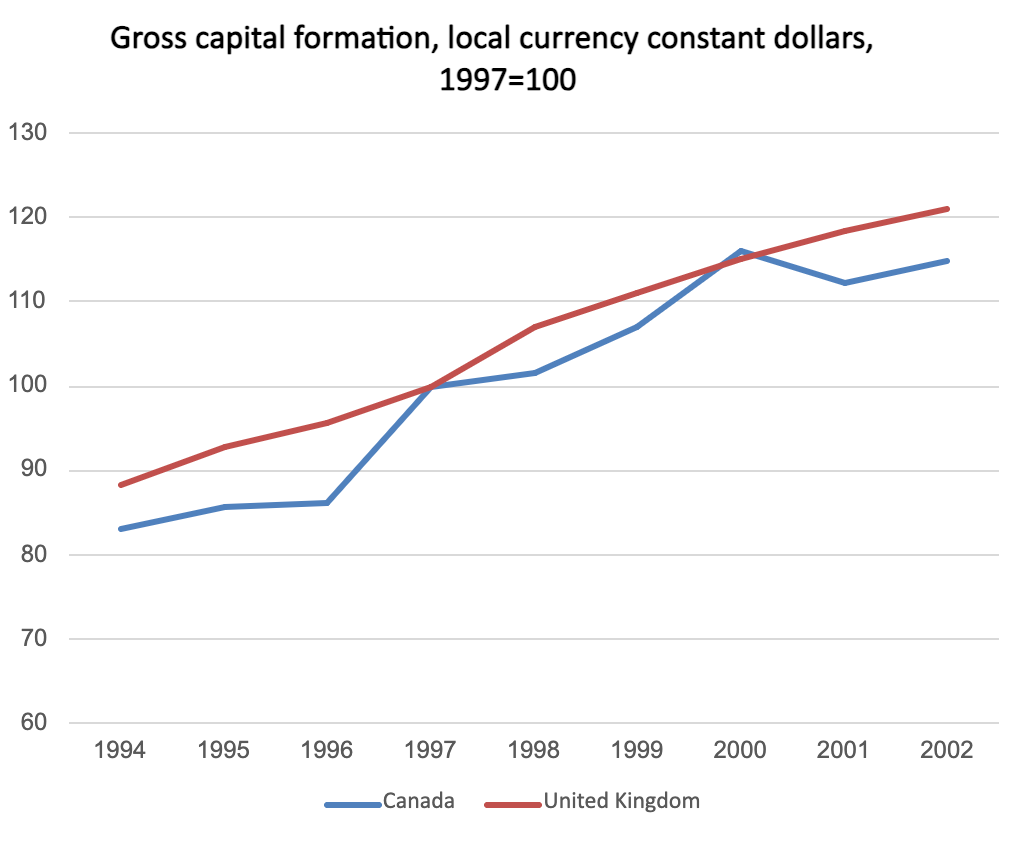

You can see this in simple terms in the following chart simply by looking at the change in fixed capital formation in Canada and the UK over the 1994-2002 period:

Following the introduction of Brown’s changes in 1997 we see a much faster growth of the capital base (including both public and private assets) in the UK compared to Canada. Since this includes dwellings during what eventually became housing crises in both countries later on, this is an imperfect way to assess things. But it does tend to be that fiscal rules such as this work in adapting behaviour to the applicable incentive structure.

In a Canadian context, my former IRPP colleague Stephen Tapp (2013) has found that fiscal rules do matter but need to be understood circumstantially. Even well-crafted rules fail without strong institutions and political buy-in. The key, he argues, is transparency and consistency, principles that sit at the core of what the Carney government is now trying to build.

What’s important to remember here is that the change proposed is simply one of categorization.

The government will break out deficit spending so that it’s clearer what portion of that deficit is composed of capital spending to create assets somewhere in the economy that support economic growth and productivity. It is NOT changing accounting rules. The public accounts will still be prepared and audited on the basis of public sector accounting rules as adapted to the federal government by the Auditor General and the Comptroller General.

This categorization can still mean a deficit and a debt that grows over time (or doesn’t go down as fast as some would like). The government will have to defend the purpose of these investments and whether they’ve accounted for them in a fair and consistent way. But the goal is to shift away from one form of spending, people and consumable services and transfers, and toward another more productive means to create growth.

How the Operating Spending Rule Will Work

At the heart of this change is the commitment that by 2028-29 there will be a balance in the operating budget. What does this mean?

The operating budget covers all recurring costs of government — program spending, transfers, administration, services, debt charges etc. — that are not about increasing value on someone’s balance sheet (either government’s own or someone else’s). Essentially everything that doesn’t fit into one of the six categories defined as capital (see below). Over time, this total level of spending must match revenue, and all future net borrowing requirements will be restricted to capital.

As discussed on our October 10 MBP Intelligence podcast, if total federal spending equals roughly 16.5 per cent of GDP and about 1.5 points of that can be classified as capital, the operating budget must be held to the remaining 15 per cent of GDP to be balanced. The small residual deficit, if any, would reflect asset-creating investments.

In other words, this isn’t about eliminating deficits altogether. It’s about structurally defining which deficits are acceptable and linking them to a tangible long-term return.

The Six Categories of Capital

Finance Canada’s backgrounder on Modernizing Canada’s Budgeting Approach identifies six categories of spending that will qualify as capital under the new framework:

- Capital transfers — transfers to governments or organizations exclusively intended for recipients to invest in infrastructure or productive assets.

- Capital-focused corporate income tax incentives — tax expenditures designed to spur new capital formation.

- Amortization of federal capital — the expense of spreading costs of federally owned or controlled capital assets over their useful life.

- Private sector research and development — direct funding or tax incentives for R&D geared toward commercialization or scaling.

- Support to unlock large-scale private sector capital investment — exceptional operating subsidies or contractual agreements that catalyze private capital projects.

- Measures to grow the housing stock — policies that accelerate new housing supply.

The controversy-prone Interim PBO Jason Jacques has criticized this definition for going further than other international norms, particularly because it could involve some things like Scientific Research and Exploration and Development (SR&ED) tax expenditures that are spent within a given year.

But maybe that’s the point? A company that is building a new patented technology is going to do this largely by employing talent who do intangible research. That patented activity is what we need more of to drive a more productive economy. Treating this expense as the same as a government worker who administers a program is ridiculous, especially when we are in a global race for AI.

And importantly, this definition doesn’t include human capital itself. So any investment in student financial assistance or training — or even child care — won’t count even if there is significant research that these investments in skills formation drive long-term productivity. The fact that the government wrote out of the definition one of the single biggest new areas of federal spending in recent decades (child care) which also arguably will deliver more GDP growth than NAFTA did should be comforting to people worried this will be a licence to spend aimlessly.

For social policy advocates the implications here are massive. This is worthy of its own follow-up, but imagine arguments for health care or homelessness funding under this new budgeting framework. The federal spending power will have to shift away from funding the human services — those consumables people need and want — and toward the infrastructure. In health care that may be fine since there is a backlog of need to build more hospitals, acquire diagnostic equipment and deploy new technology and AI tools. But in other areas it may necessitate a coordinated shift in spending priorities to ensure that this new approach doesn’t crowd out still necessary investments in frontline service delivery for things like child care, addictions counselling, employment support and other core human services.

What’s also interesting are the edge cases. These will be examined in future installments of this series. Things like nature and housing.

Fixing Canada’s under-investment in itself

At its core, this reform is about reversing a national trend of under-investment.

When Gordon Brown introduced the golden rule in 1997, the UK faced an investment drought. Non-residential capital spending had risen only about seven per cent in real terms over the previous three years. Canada today is in the opposite position — its non-residential investment has fallen roughly seven per cent since 2021, according to OECD data.

By explicitly reserving deficits for asset-creating investments, the Carney government is aiming to rebuild the country’s productive base and crowd in private capital. Borrowing, in this model, becomes a lever for future capacity, not a tool for present consumption.

Why this is more than a fiscal anchor

This new framework should not be confused with a “fiscal anchor” in the conventional sense — it’s a behavioural rule. Fiscal anchors set numerical targets for debt or deficit ratios. And we may yet see a specific set of objectives on that front in the Budget. Behavioural rules change how governments decide what counts as legitimate spending in the first place.

Experience from the UK and other OECD economies suggests such frameworks can raise investment and productivity — but only if definitions stay clear and oversight stays strong. The golden rule worked because the UK paired it with transparent reporting and independent verification through the Office for Budget Responsibility. Canada’s credibility will depend on similar transparency.

Taken together, this first set of reforms reveals a lot about Mark Carney’s governing instincts:

First, he values fiscal transparency. By drawing a clear line between operating and capital budgets, the government is making visible what used to be buried — whether deficits are paying for daily programs or long-term investments. This should hopefully help Canadians better understand how their money is spent. But that relies on sharp Budget communications — experience would suggest that is hard to do.

Second, he values coherence. Carney’s reforms are internally consistent — the rule, the institutional machinery, and soon the new budget calendar all reinforce one another. Each is designed to make policymaking more disciplined and rational. The fiscal policy lever is being used purposefully to address the core macroeconomic concern — how to get more investment moving.

Time will tell whether Canadians prefer investing in building roads versus the added presence of police or social services to address crime on our streets. Or whether more nurses and doctors are more or less important than AI patents. Both matter, and Canadians will likely want both. But only one kind wins out under this new budgeting approach and departments and stakeholders will inevitably respond to those incentives over time.

Third, he still looks to the UK as a guidepost. The golden rule, the capital-operating distinction, and soon the shift to a fall budget all trace to lessons from British fiscal reforms. That through-line says something about Carney’s philosophy.

Ultimately, this first wave of Carneynomics is not about the eventual hard choices of what to cut and what to invest in. It’s about structure — and arguably aligning government to how public companies themselves make decisions about how to allocate capital. For those thinking “spending is spending” — you’re missing the big picture.

If this shift in budgeting has the intended effect of spurring on private sector investment and raising our long term economic growth path higher than today, it could rebuild both public trust and Canada’s capacity to invest in itself.

Next in this series: how shifting the federal budget to the fall will rewire the internal timings of departments, reordering incentives, and creating new accountability dynamics.